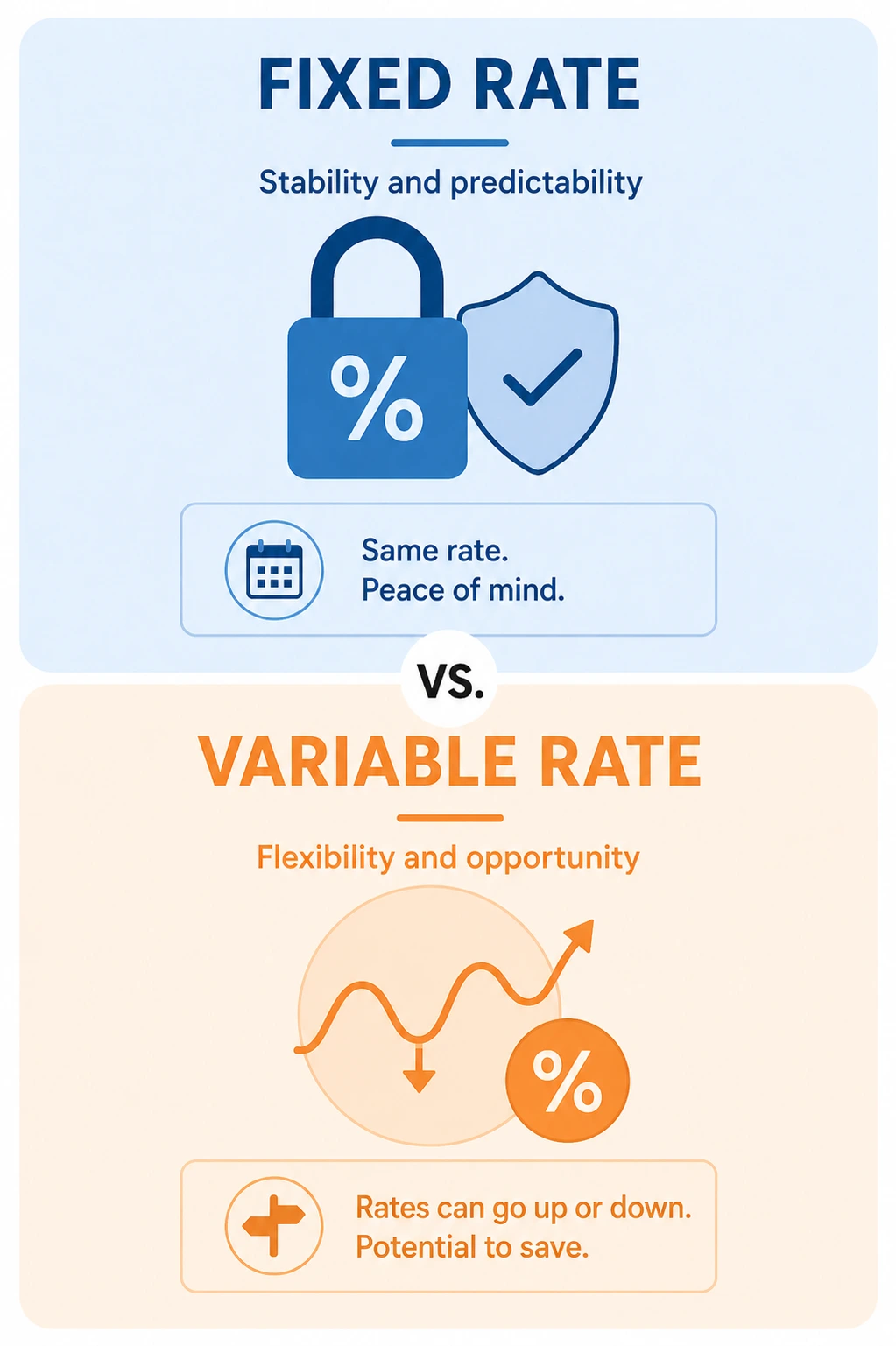

Fixed or Variable?

You Decide.

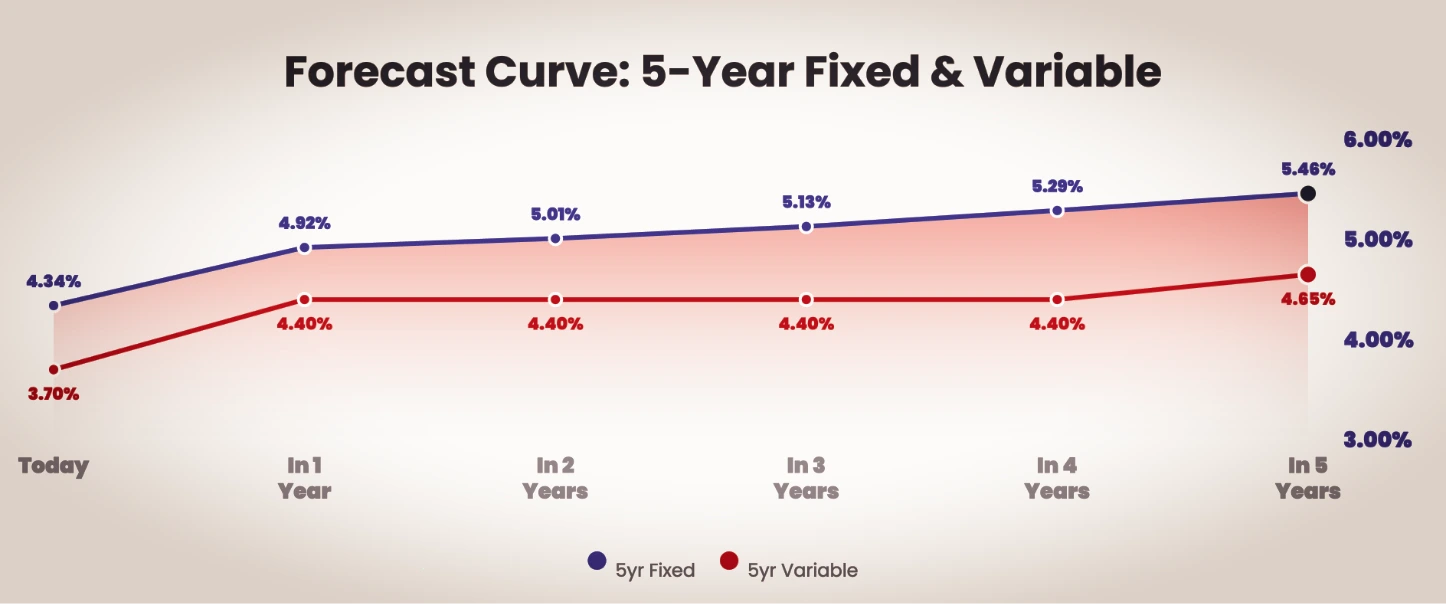

Based on today’s forecast, variable rates trend lower over the next five years.

Variable starts cheaper and stays cheaper through the 5-year term – giving you more room in your budget today and meaningful savings if the forecast holds. Fixed trades that savings advantage for the security of a predictable payment. Here’s what today’s numbers look like over a 5-year term.

Two Approaches to the

Same Monthly Payment

Variable starts cheaper – giving you more room in your budget today. Fixed trades flexibility for the security of a predictable payment. Here’s what today’s numbers look like over a 5-year term. These projections are based on current market conditions and subject to change—speak with Bruno to discuss what makes sense for your situation.

- Your payment never changes for 5 years – even if the Bank of Canada raises rates overnight

- Built-in insurance against rising rates; you sleep well regardless of economic headlines

- Predictability means you can budget your household with zero guesswork

- Starts lower than fixed today – potentially saving thousands if rates rise slower than expected

- Market pricing suggests rates will rise gradually over the next 5 years

- You benefit when rates stay flat or rise slower – but absorb the cost if they climb faster than forecast

Side-by-Side Comparison

No opinion, no sales pitch. Just the facts so you can weigh what matters most to your situation.

| 5-Year Fixed | 5-Year Variable | |

|---|---|---|

| Starting Rate | 4.34% — locked for 5 years | Typically lower than fixed at inception |

| Payment Stability | Unchanging for the full term | Fluctuates with the prime rate |

| If Rates Drop | You stay at 4.34% | Your payment goes down with it |

| If Rates Rise | You’re protected at 4.34% | Your payment increases |

| Forecast Over 5 Years | Market suggests rates trend lower – but forecasts aren’t guarantees | |

| Best For | Peace of mind & budget certainty | Comfort with risk & potential savings |

Who Should Go Fixed? Who Should Go Variable?

Choose Fixed If You…

- Want your housing cost locked in and predictable for 5 years, no matter the economy

- Understand your penalty risks upfront and prefer certainty over flexibility

- Are uncomfortable with market uncertainty and prefer paying a small premium for certainty

- Have a tight budget where even a modest rate increase would cause stress

- Prefer to set it and forget it & no checking headlines every rate announcement

- Value sleep quality over potential savings

Choose Variable If You…

- Believe rates will rise gradually and want to benefit if they climb slower than expected

- Have an understanding of economic cycles and events and can adjust your strategy accordingly

- Have enough room in your budget to absorb a rate increase if the forecast is wrong

- Would be willing to accept a variable rate with a static payment for a bit of added stability

- Want the lowest possible starting rate and maximum flexibility

- Only 3-month interest penalty to break the mortgage

- No charge to convert to a fixed-rate payment if market conditions change

The reality: Neither is objectively “better.” The right choice depends on your risk tolerance, budget flexibility, and outlook. And in today’s market, the gap between fixed and variable is narrow enough that the decision comes down to what keeps you comfortable – not a dramatic savings either way.

Current snapshot as of May 2026 – subject to change with market conditions.

Still Not Sure Which Is

Right for You?

Book a free 15-minute call. Walk through your numbers together, weigh the forecast against your real situation, and walk away knowing exactly what makes sense – no pressure, no obligation.

No obligation. We’ll see if we’re a fit.